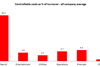

Payroll costs now equal 26% of average turnover

Payroll costs for licensed retailers increased from 24.2% of turnover in 2013 to 26.4% last year, according to the latest benchmarking report from the Association of Licensed Multiple Retailers.

Already have an account? Sign in